FinanceGraphs

A flexible wrapper around dygraphs and ggplot2 to graph and annotate

financial time series data.

The package provides several ways to add additional information to a

simple series vs time data, including horizontal annotations (events

highligted by lines and colored bands) and vertical annotations (key

levels or regions). Colors and set of labels can be customized and

persist across invocations of the package, but sensible defaults are

used. To minimize verbiage to get what you want, the package emphasizes

options in the main function call rather than multiple functions or

pipes to build up a graph.

You can install the development version of FinanceGraphs from

pak::pak("derekholmes0/FinanceGraphs")

# install.packages("FinanceGraphs") # If from CRAN

Dygraphs for time series

The package is designed to be flexible with input data. The data can

either be in long format

(e.g. date,series,value) or

wide format

(date,col1,col2,…).

The date column can be called anything or be anywhere in

the input data.frame, but there must be at least one coercible column

with dates and one numeric column. Each column after the date column is

treated as a separate series to be graphed, but if the column name

(series name) ends in any of ‘.lo, .hi,

.f (for forecast),’.flo, .fhi

then those columns are treated specially as lower/upper bands or

forecast series associated with the prefix of the name.

Consistent colors used for all series and annotations are kept in a

local (persistent) settings data.frame. Default color

schemes can be changed (again persistently) using the

fg_update_aes() function.

Simple Examples

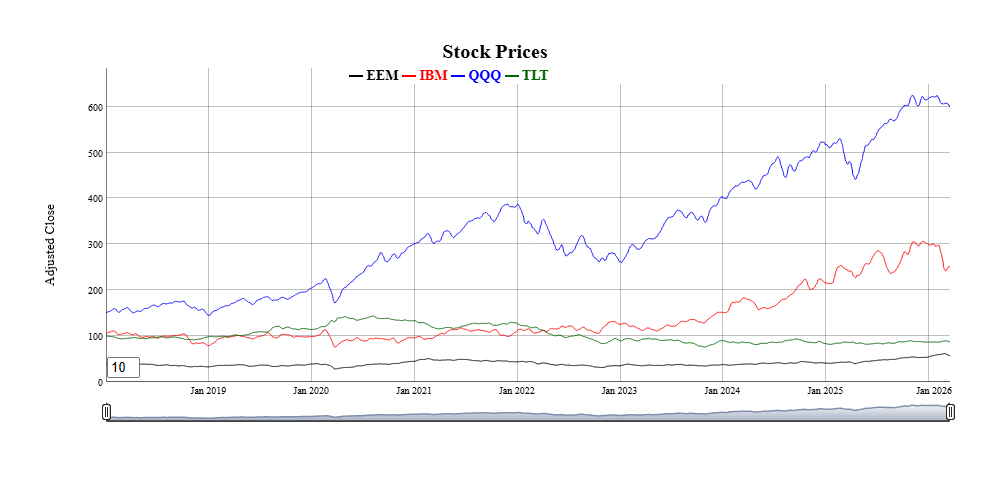

fgts_dygraph(eqtypx, title="Stock Prices", ylab="Adjusted Close")

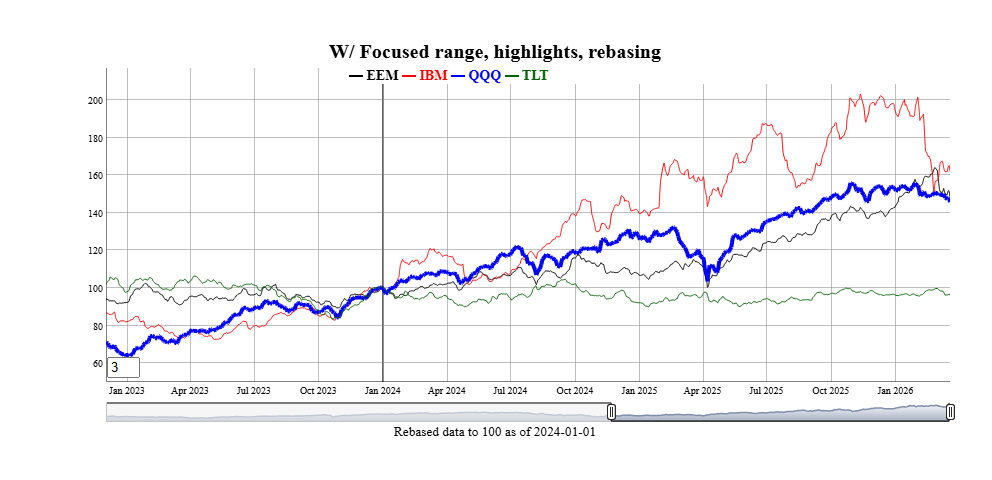

* All of the data is displayed on the graph by default, but nost of the

time, we want to focus on recent periods and have the option of backing

up to all history. The

* All of the data is displayed on the graph by default, but nost of the

time, we want to focus on recent periods and have the option of backing

up to all history. The dtstartfrac parameter shows just the

last (1-dtstartfrac) percent of the data. Alternatively, a

generic date window of the form “start::end” can be used in the

dtwindow parameter. Each end of the window can be a full

date (e.g. “2022-01-01”) or a relative date string (e.g. “-6m” for 6

months ago.

One of the most appealing features of dygraphs is the ability to smooth

series interactively. The roller parameter adds a rolling

average smootherof the specified width (in data points). A default

smoothing parameter is chosen depending on the length of the underlying

data, but can be overridden using the roller

parameter.

Individual series can be altered in several ways:

- Highlighted with different stroke patterns and width using the

hilightcols argument with a string (possibly list) of

series names, hilightwidth for a new width, and

hilightstyle for a new stroke pattern.

- Shown a step plot using the

stepcols argument with a

string (possibly list) of series names.

- Hidden from using the

hidecols argument with a string

(possibly list) of series names.

- Rebased to a given constant at a particular date.

fgts_dygraph(eqtypx, title="W/ Focused range, highlights, rebasing",

dtstartfrac=0.6,hilightcols="QQQ",hilightwidth=4,rebase="2024-01-01,100",roller=3)

Series can be grouped together into bands by adding new columns

in the data with names ending in ‘.lo’ and

‘.hi’ for lower and upper bounds. Those additional series

can represent many things, such as statistical extremes, rolling

correlations to other variables (see vignette), or (as a special case)

forecast confidence intervals.

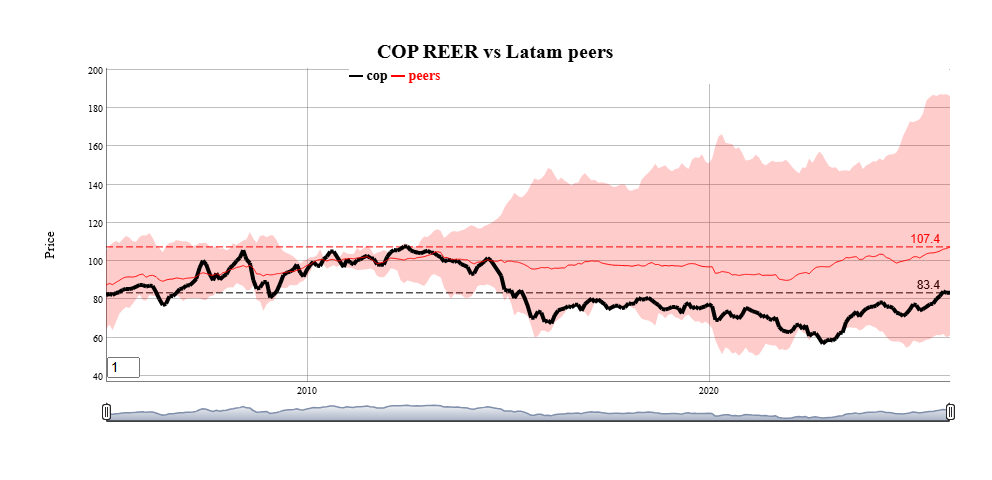

Horizontal annotations can also be added using the

annotations parameter. The most common example is a

horizontal line at the last observations of each series.

toplot <- reerdta[REGION=="LATAM",.(cop=sum(value*(variable=="COL")),

peers=mean(value),peers.lo=min(value),peers.hi=max(value)),by=.(date)]

fgts_dygraph(toplot,title="COP REER vs Latam peers",ylab="Price",

roller=1,hilightcols="cop",hilightwidth=4,annotations="last,linevalue")

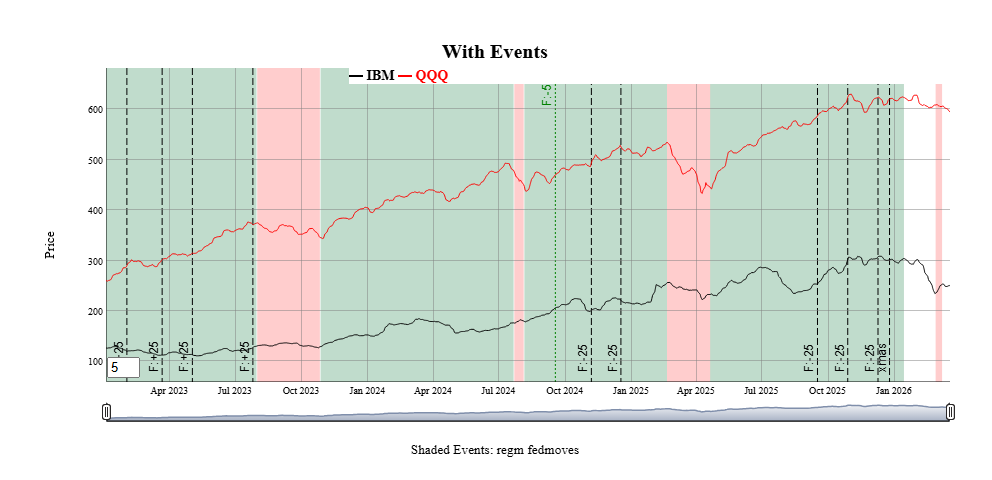

Events

Annotations to a particular date or date range can be added to the

graph using the events and event_ds

parameters.

The events parameter is a string with one or more

(separated by semicolons) event specifications. The

event_ds parameter is an optional data.frame with user

defined events. (See Vignette for examples) Any events specified with

either parameter are additive.

Events in the function call

Events always have a start date and a text label. THey are shown as

vertical lines on the graph unless they also have an End Date, in which

case the entire region is shaded. Event strings starting with

doi (date of interest) are predefined events included with

the package. Those are customizable using the

fg_update_dates_of_interest() and can be listed using

fg_list_dates_of_interest(). Event strings can be added

together with semicolons, as in the following example:

smalldta <- eqtypx[date>=as.Date("2023-01-01"),.(date,IBM,QQQ)]

fgts_dygraph(smalldta,title="With Events",ylab="Price",events="doi,regm;doi,fedmoves;date,xmas,2025-12-25")

Several types of events are predefined in

Several types of events are predefined in fgts_dygraph()

including equity option expirations, IMM CDS roll dates, seasonal events

(e.g. “same day in quarter as last observation”) and series extremes.

See the vignette for more examples. Events can also be passed in as a

data.frame using the event_ds parameter, as

shown next.

Event helpers

Custom events can also be passed in data.frame format

using the event_ds parameter. The details are in

fgts_dygraph(), but the basic columns are a start date

date, a text label, and if applicable an end date. Only events within

the dates of the original input data are shown.

The package includes a few “event helpers” to make it easy to

generate the right formats for given more complicated types of events

and exogenous data. See the vignette for examples, but here is an idea

of two that can be done.

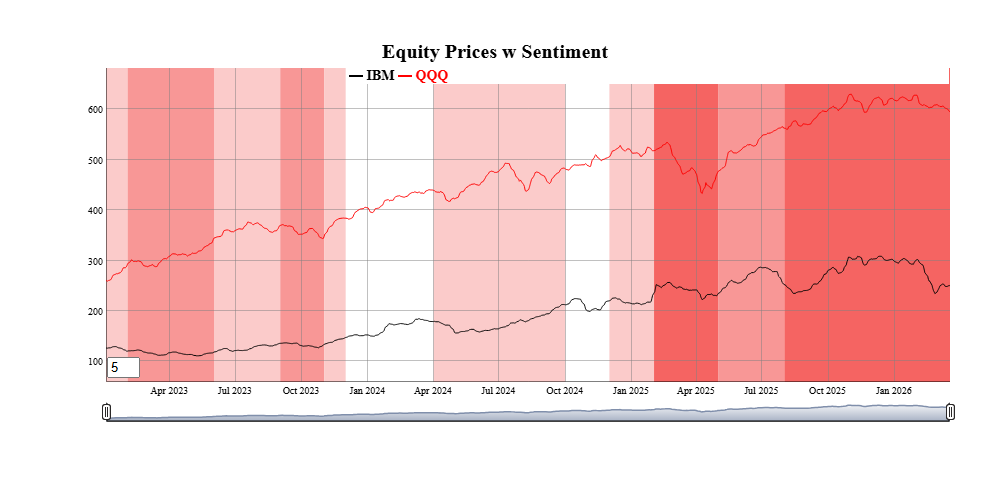

events_consumer_sent <- fg_cut_to_events(consumer_sent,center="zscore")

head(events_consumer_sent,2)

#> value color END_DT_ENTRY DT_ENTRY runlen

#> 1: 3 #9595FFFF 2016-03-02 2016-01-01 3

#> 2: 2 #CACAFFFF 2016-04-02 2016-03-02 1

fgts_dygraph(smalldta,title="Equity Prices w Sentiment",event_ds=events_consumer_sent)

Current event helpers are:

Current event helpers are:

fg_findTurningPoints() |

Statistically identify turning points in a

series |

fg_ratingsEvents() |

Add colored ranges based on analyst credit

ratings |

fg_cut_to_events() |

“Cut” a univariate series into colored

bands, with two different colors for positive and negative values |

fg_signal_to_events() |

Map a long/short signal to events |

fg_tq_divs() |

Add dividend events from TidyQuant

dividend data |

fg_av_earnings() |

Add earnings events from AlphaVantage

earnings data |

Forecasts

Forecasts beyond the last day of the dataset can also be added in a

consistent way. For example, forecasts (and confidence intervals) for

the IBM stock price in new data.frame can be added as

follows. Each forecast is shown as the same color as the original

series, but dashed to show the transition.

head(example_fcst_set,2)

#> date QQQ.f QQQ.flo QQQ.fhi IBM.f IBM.flo IBM.fhi

#> 1: 2026-03-21 582.8459 574.5719 591.1199 241.965 236.1769 247.7531

#> 2: 2026-03-22 582.8459 571.5502 594.1416 241.965 233.8706 250.0593

fgts_dygraph(smalldta,title="With Forecasts", dtstartfrac=0.7,forecast_ds=example_fcst_set)

Like events, forecasts can be generated from many packages with

different output formats. There is also a “forecast helper” to get their

outputs into the appropriate foreast_ds forms

Changing

aesthetics and adding “dates of interest”

Default colors for series and annotations can be changed using

fg_update_aes() or fg_update_line_colors().

Any changes made to aesthetics colors will persist across loads of the

package (unless persist=FALSE is specified). To see what

aesthetics are used for any particular function, use

fg_print_aes_list() As an example, to make a graduated set

of colors for the first 2 series.

fg_get_aes("lines",n_max=2)

#> category variable type value const used helpstr

#> 1: lines D01 color black all Low cardinality line colors

#> 2: lines D02 color red all Low cardinality line colors

fg_update_line_colors( rev(RColorBrewer::brewer.pal(8,"GnBu"))[1:2] )

#> Saved aesthetic updates to C:\Users\DFH\AppData\Local/R/cache/R/FinanceGraphs/fg_aes.RD

fg_get_aes("lines",n_max=3)

#> category variable type value const used helpstr

#> 1: lines D01 color #08589E all Low cardinality line colors

#> 2: lines D02 color #2B8CBE all Low cardinality line colors

#> 3: lines D03 color blue all Low cardinality line colors

New dates of interest used for the events parameter can

also be added. To add (for example) a new FOMC cut of 50bps on 6/16/2026

(after the development of this package), use

fg_update_dates_of_interest(). Resetting the lists (and

colors) can also be done.

newdoi <-data.frame(category="fedmoves",eventid="F:-50",DT_ENTRY=as.Date("6/16/2026",format="%m/%d/%Y"))

fg_update_dates_of_interest(newdoi)

#> Saved dates of interest file to C:\Users\DFH\AppData\Local/R/cache/R/FinanceGraphs/fg_doi.RD

#> NULL

tail(fg_get_dates_of_interest("fedmoves"),2) |> data.frame()

#> category eventid eventid2 DT_ENTRY END_DT_ENTRY color strokePattern loc

#> 1 fedmoves F:-25 rt:4 2025-10-29 2025-10-29 <NA> <NA> <NA>

#> 2 fedmoves F:-25 rt:3.75 2025-12-10 2025-12-10 <NA> <NA> <NA>

fg_reset_to_default_state("all")

#> Removing dates file and reverting to defaults of package

#> Removing Aesthetics file and reverting to defaults of package

#> Removing User-made Themes and reverting to defaults of package

#> Removing cache Directory

#> fg_reset_to_default_state(all) completed

Integration into Markdown

and Shiny

Dygraphs have the very nice feature of allowing synchronized zoom in

Markdown or Shiny applications. Each graph with a common

group identifier is synchronized. There are times, however,

when you want to turn these on or off. The function

fg_sync_group() either returns the current group name if

called with no parameters, sets the group name with a string, or turns

off synchronization with a call fg_sync_group(NULL).

Static Plots for Time Series

Scatter Plots

with time dimension enhancements

Key to understanding how time series co-move is a simple scatter

plot. The function fg_scatplot() tries to be a concise

wrapper around the very comprehensive ggplot2 graphics framework.

ggplot2() is a great ecosystem, but requires quite a bit of

verbiage to get from idea to presentable graph quickly. The approach

used here is to specify broad categories of aesthetics with a formula,

while the details are kept behind the hood using the aesthetic sets

managed by fg_get_aes() as above. Fuller explanations and

more examples are in the accompanying vignette.

This “one-line” approach can be used with both date-based and

non-date based datasets. For example, suppose we wanted to plot two

asset prices against each other so that we can easily understand both

how they co-move, where they have been recently, and where they are now.

We will start by making a fake dataset of two sets of two assets

each.

set.seed(1)

ndates <- 400;

samp_rw <- function() { 100*(1+cumsum(rnorm(ndates,sd=0.2/sqrt(260)))) }

dts <- seq(as.Date("2021-01-01"),as.Date("2021-01-01")+ndates-1)

dttest <- rbind( data.table(date=dts,ccat="A",px_x=samp_rw(),px_y=samp_rw()),

data.table(date=dts,ccat="B",px_x=samp_rw(),px_y=samp_rw()))

A scatter plot of where those two assets are and where they have been

is as easy as specifying (in one string!) columns to plot, a column for

color, and a term to split the dates into 2 month and 6 month intervals,

and finally a term to show where the latest observations are. As with

fgts_dygraph(), date partitions can be custom regimes

managed by fg_update_dates_of_interest().

fg_scatplot(dttest,"px_y ~ px_x + color:ccat + doi:recent + point:label","lmone",datecuts=c(60,182),title="Splitting dates")

One important feature of the static plots in this package to note is

that they include options for switching the colors of large numbers of

groups or points from discrete values to continuous values from the RColorBrewer package.

One important feature of the static plots in this package to note is

that they include options for switching the colors of large numbers of

groups or points from discrete values to continuous values from the RColorBrewer package.

fg_scatplot() does not require dates in the input data,

and can be useful for communicating comparative analyses as well. The

mtcars dataset shows how we can add a lot of information to

a basic text scatterplot.

dt_mtcars=data.table(datasets::mtcars)[,let(id=lapply(rownames(datasets::mtcars),\(x) last(strsplit(x," ")[[1]])))]

fg_scatplot(dt_mtcars,"disp ~ hp + color:carb + label:id","lmonenoeqn",n_color_switch=0,title="Text with color switch")

Many more examples that encapsulate a large part of the ggplot2 corpus are in the

accompanying vignette.

Time-categorized box plots

One way to visualize multiple time series comparatively with a

boxplot or a violin plot. The function fg_tsboxplot()

provides a flexible way to split several time series into time

categories. Usually, those categories are time periods with increasing

horizons, but this function allows for arbitrary periods managed by

fg_update_dates_of_interest(). Data can be normalized

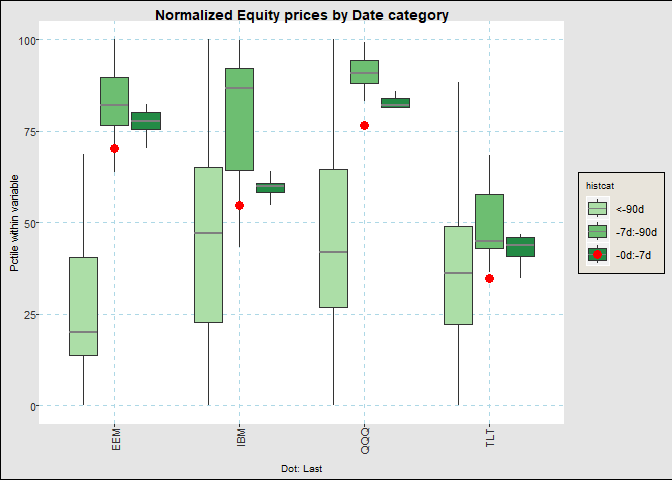

across historical categories and time series categories. As an example,

suppose we would like to see normalized equity prices over the past two

years, split into categories of the last week, month (less the last

week) and the last quarter.

fg_tsboxplot(narrowbydtstr(eqtypx,"-2y::"),breaks=c(7,90),normalize="byvar",title="Normalized Equity prices by Date category")

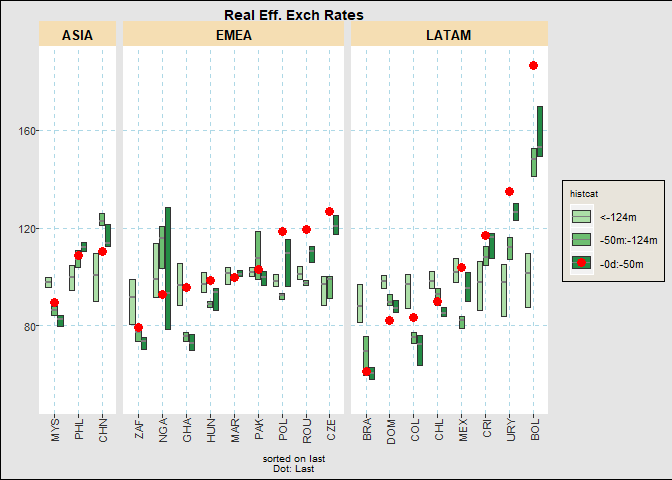

Like fgts_dygraph(), the function can take data in both

wide and long formats. Longer formats have the advantage of adding more

categorical levels to our graphs. For example, we can plotting recent

ranges of the monthly FX Real Exchange Rate dataset in the following

way. Here, we split the data into buckets of last 20pct of the months,

the first half the months and the last. We will also show the last

observation, hide the boxplot whiskers, and reorder the currencies by

their relative weakness.

fg_tsboxplot(reerdta,breaks=c(0,0.2,0.5,1),doi="last",orderby="value",boxtype="nowhisker",facetform=". ~ REGION",title="Real Eff. Exch Rates")

Event Studies

Trying to understand how events or environments may impact prices can

be summarized well by plotting their movements relative to a date

against time relative to the event. The function

fg_eventStudy() integrates a set of dates with a set of

time series to plot their relative behavior over the business days

before and after each event. It is designed to show reasonably large

sets of assets or event dates by switching discrete color scales to

gradient scales after a user specified number.

There are several ways to show the data, including path-by-path,

statistics by event (i.e. across assets) or by asset (across events),

boxplots, or scatter plots of moves at the edge of the intervals.

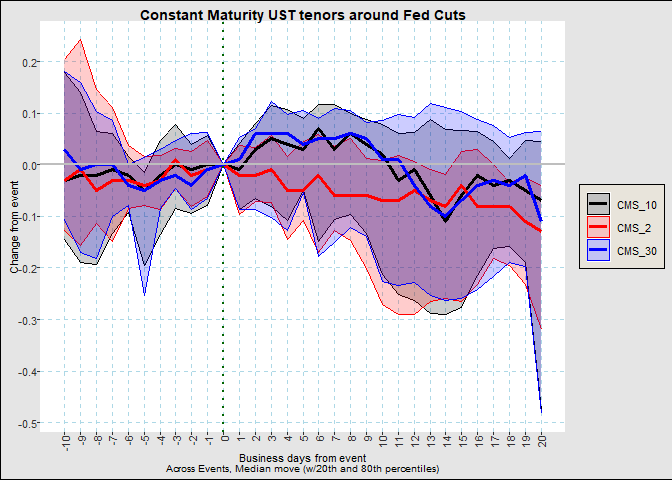

For example, to see the behavior of various parts of the US yield

curve around FOMC cuts, just use the following

dtset <- fg_get_dates_of_interest("fedmoves")[grepl("F:-",eventid),.(DT_ENTRY,text=eventid2)]

fg_eventStudy(yc_CMSUST,dtset,output="pathbyvar",

title="Constant Maturity UST tenors around Fed Cuts")

We can see that curves reach their peak steepening around a week

after the event. To see this a little more succinctly, we can use

fg_eventStudy(yc_CMSUST,dtset,output="scatter",nbd_back=5,nbd_fwd=6,

title="Constant Maturity UST tenors around Fed Cuts at 5 days")